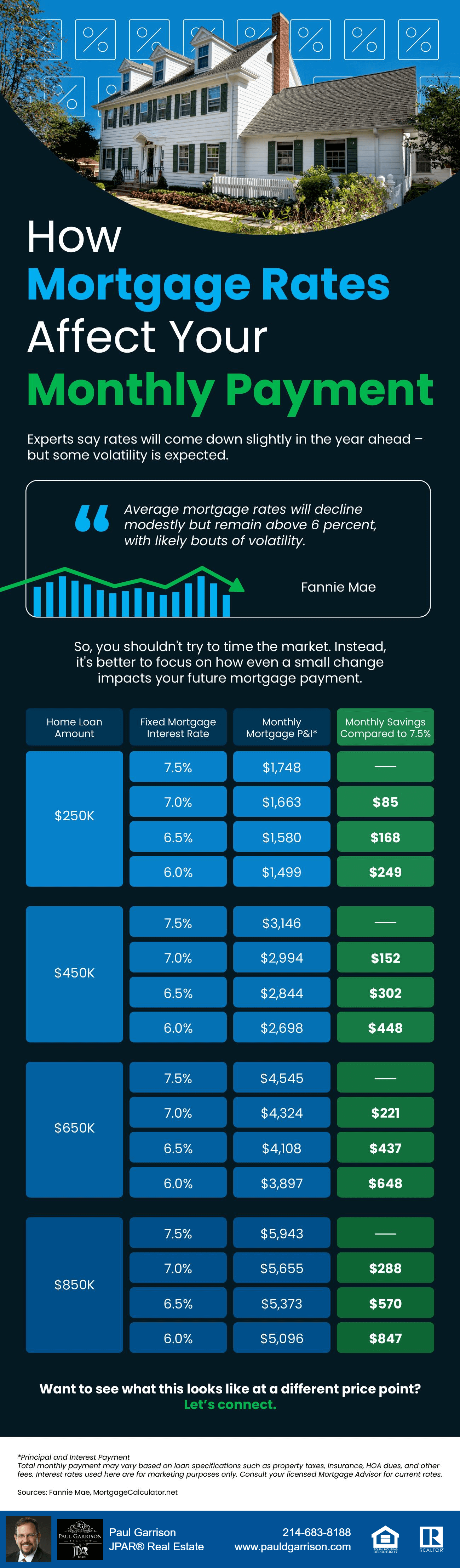

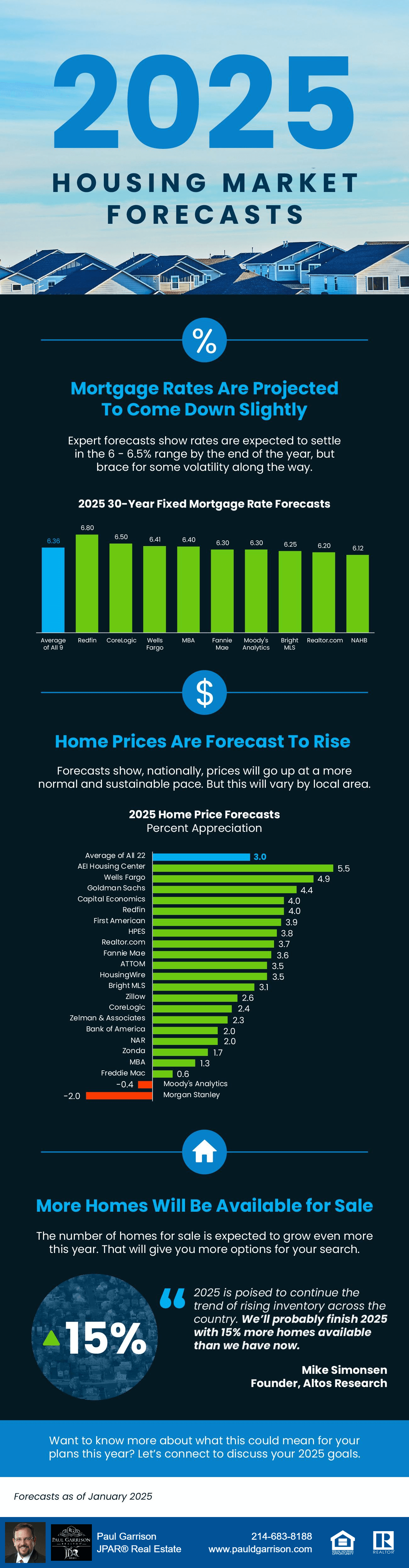

Wondering what to expect when you buy or sell a home this year? Here’s what the experts say lies ahead. Mortgage rates are projected to come down slightly. Home prices are forecast to rise in most areas. And, there will be more homes available for sale. Want to know more about what this could mean for your plans this year? Let’s connect to discuss your 2025...