You’ve probably seen the headlines saying, “foreclosures are on the rise,” and maybe your mind jumped straight to 2008. That’s understandable. A lot of people remember that crash and all the foreclosures that happened during that window, and they’re hoping something like that never happens again.

But this isn’t a repeat of what happened back then. Here’s the context to prove it.

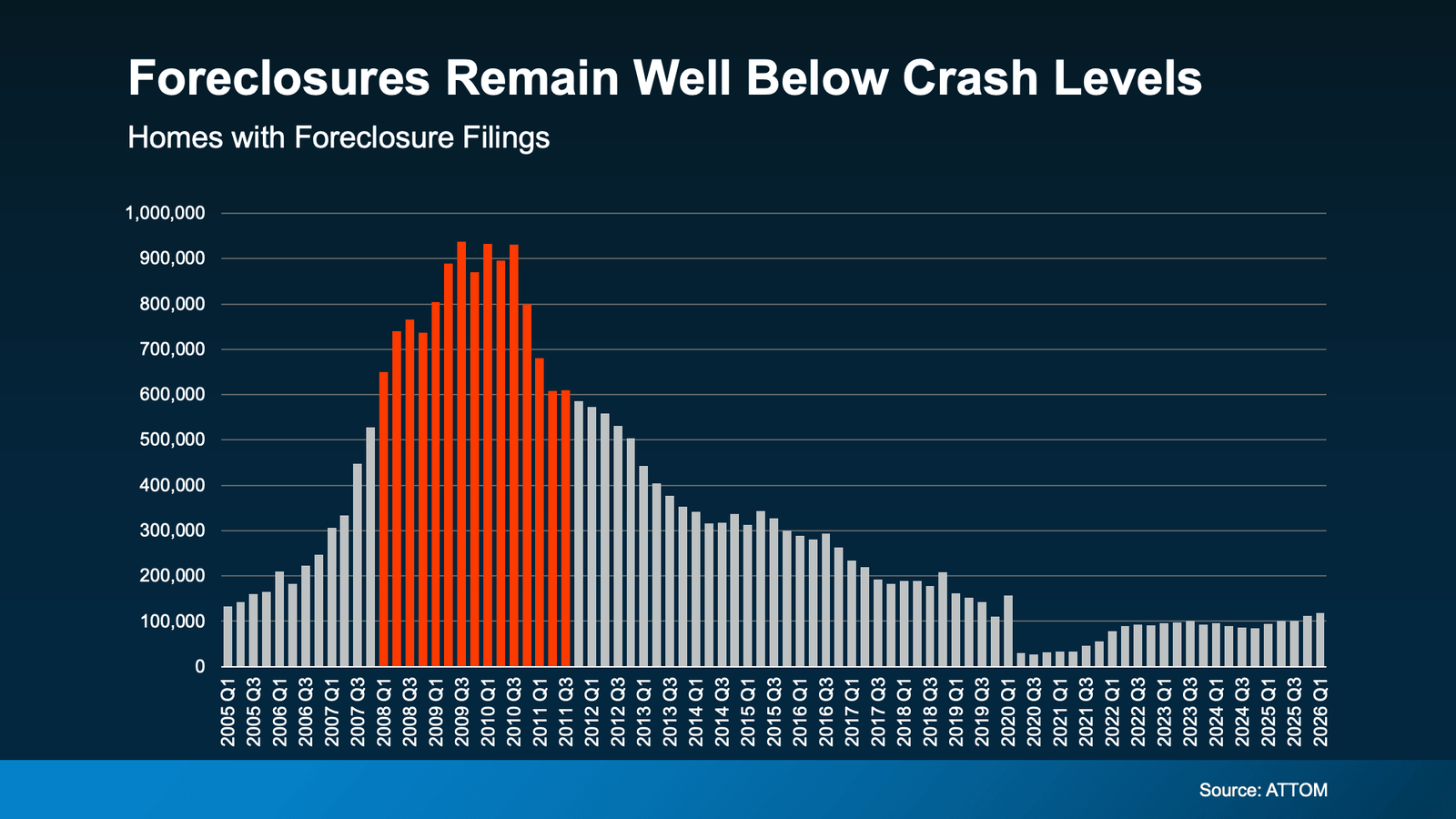

Foreclosures Are Rising, But They’re Still Historically Low

Yes, foreclosure filings are up 26% from a year ago, according to ATTOM. And they’ve been rising for 5 straight quarters. That’s a real trend worth paying attention to. But the full picture isn’t scary like the headlines suggest.

The reality is the increase we’re seeing is a sign of the market normalizing.

Here’s an important thing to know about this chart. The extremely low numbers you see in 2020 and 2021 don’t represent what’s “normal.” That’s when the government put a moratorium on foreclosures to help homeowners get through the pandemic. Those years were an exception, not the baseline.

Instead, compare where we are today to 2017, 2018, and 2019 – the last years the market was running normally. Today’s numbers are still lower. So, we’re not even back to what’s typical, yet. That means this can’t be a crash. (see graph below):

While today’s numbers are getting closer to pre-pandemic levels, they’re still below historical norms. And just look at what was happening around 2008. Even with the recent increase, we’re nowhere near those levels. This is a market returning to normal, not heading toward a crisis.

Why Today’s Equity Picture Changes Everything

Most of those filings won’t even end in a completed foreclosure. That’s because today’s homeowners have something most people in 2008 simply didn’t have. And that’s equity.

The average homeowner today is sitting on roughly $295,000 in home equity right now, according to Cotality. Back in 2008, many people owed more than their homes were worth. Selling wasn’t an option. And foreclosure was often the only door available.

Today, that’s not the case. If you have enough equity to cover what you owe and the cost of selling, you could sell your home, pay off your debt, protect your credit, and potentially walk away with money in your pocket.

That’s a completely different situation than what homeowners faced during the last crash, and it’s a big reason we’re unlikely to see foreclosures spiral the way they did back then.

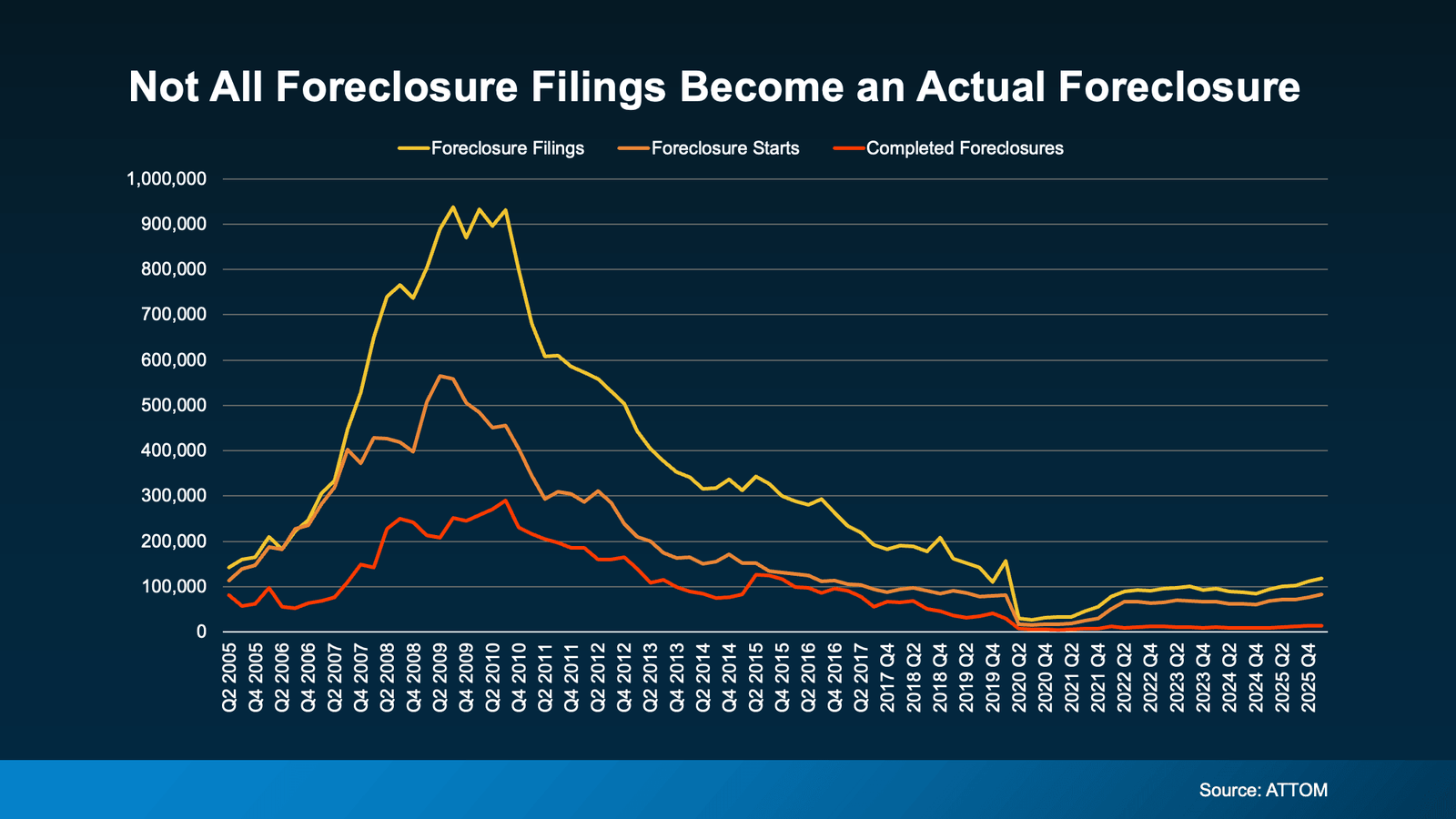

Check out the graph below. It shows foreclosure data from ATTOM going back to 2005. Here’s how to read it:

- The yellow line tracks all foreclosure filings.

- The orange line tracks foreclosure starts, meaning the process has officially begun.

- And the red line at the bottom tracks completed foreclosures (the ones where a homeowner actually lost their home).

See how the red line stays well below the other two? That gap tells the real story. A lot of homeowners who enter the foreclosure process never end up losing their home because they find another way forward first.

Today’s equity is a big reason for that. So, even the filings we are seeing now won’t all end in foreclosure.

If You’re Struggling, You Have More Options Than You Think

Maybe you’re behind on payments. Maybe you’re stressed about what comes next. That’s an incredibly hard place to be, but it’s important to know that missing a payment or two doesn’t automatically mean you’ll lose your home.

Banks would much rather work with you than foreclose. It’s a complicated, costly process for them, too. They’re often willing to set up a repayment plan, offer forbearance (a temporary pause or reduction in your payments), or modify your loan to make things more manageable long-term.

Just know the sooner you reach out to your lender, the more options you’ll have. In some states (ones that don’t require the foreclosure process to go through a court) things can move faster than people expect. Getting ahead of it early gives you and your lender the most room to find a solution.

And if selling makes more sense for your situation, a real estate agent can help you understand what your home is worth and whether that’s a path worth exploring.

Bottom Line

Foreclosure filings may be rising, but they’re still low. And the equity most homeowners are sitting on today is a key reason this looks nothing like 2008.

Join The Discussion